A few months ago, I wrote about How Financial Statements Are Born, which explained how different financial statements were related to one another. A supplement to that is a How To Be A Financial Detective presentation that Thomas Blaney and Christopher Peterman made at a Grant Managers Network conference.

This presentation is generally focused on educating board members and potential donors about how to interpret different non-profit financial statements.

Obviously then, there are tips in the presentation that non-profit administrators can employ to make their financial reporting more effective at reflecting the state of their organization. Not to mention providing the organization with a greater understanding of the reports themselves.

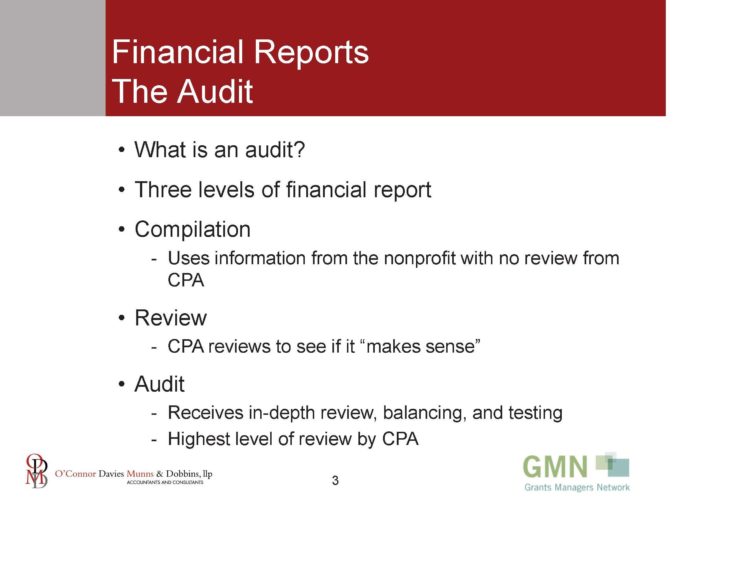

For instance, are you aware of the three levels of financial report review?

Non-profits often depend heavily on in-kind donations of goods and services. However, you may not be aware that the donation of services must meet specific criteria:

One of the following conditions must be met:

•Services create or enhance non-financial assets (such as a building)

•Services must meet all three of the following:

1. Require specialized skills

2. Are provided by someone with those skills, and

3. Would have to be purchased if they were not donated

By these criteria, if an architect donates his/her design services, you can report it as an in-kind donation of services. If the architect ushers for a show, you can’t.

For board members who are used to dealing with the statements and operations of for-profit corporations, the presentation may be especially helpful because it illuminates many of the differences between the way resources are allocated and evaluated for programs and how funding and budgeting are handled.

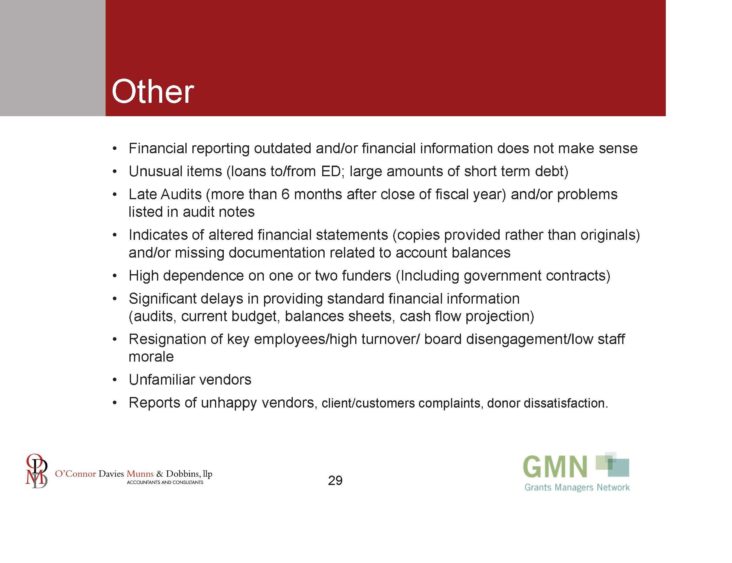

For example, loans to the CEO by the corporation he/she directs are not uncommon, but are red flags for non-profits. Short term debt is also viewed differently in a corporate setting than in a non-profit one.

The importance of good governance is an increased focus in the non-profit sector. Understanding financial documents is one of the more challenging aspects of this duty for many board members. If you are able to offer resources like this presentation which tells board members what to pay attention to in financial documents, and the presentation in my previous entry that illustrates how the different financial documents relate to each other, you have a reasonably good primer on the subject.

Thank you for the authoritative read on this issue. To me, being able to actually see the icon in the…